An established player for sheet vinyl floorings, polyvinyl chloride (PVC) films and sheeting, and artificial leather in India, growing at 14% CAGR for the last 10 years and growing at 20% CAGR for the last 3 years. The company boasts an extensive marketing network comprising 90 to 100 dealers strategically positioned across India. Additionally, they have cultivated strong and enduring relationships with end-users. The company extends its global reach by exporting its products to more than 25 countries worldwide. Available at less than 1x Sales and 15x earnings.

About the Company

Premier Polyfilm Ltd. (Mcap 200 Cr) is one of the leading manufacturers and exporters of calendered PVC products. The company with an experience of 25 years in producing PVC products as per international Quality Standards. The products meet EN, ISI & ISO requirements of Fire and smoke and Abrasion resistance, etc.

Products:

Their range of products includes PVC Flooring, PVC Sheeting, PVC Flexible Film, Calendared Leather cloth, PVC Geomembrane, High voltage Insulated Mats etc.

The company markets their products under the brand names Polychallenger, Polyfloor, Polyfabs, Electromat & Aqualining

Applications:

The products of the company are used for a variety of industrial and consumer applications e.g., PVC products, Transport Flooring with Silicon Carbide Flooring for Heavy Traffic applications, Artificial Leather, 100% Shockproof insulating Mats for Buses and Cars, PVC Sheeting for Table Covers

Research & Development:

Continuous development of economical formulations of the above R&D has helped the company to reduce the cost of manufacturing. By introducing a new range of colour schemes and designs of finished products the Company’s products continue to be in demand.

The Company has been spending some percentage of revenue on R&D since 2011. This helped the company to build a strong brand in the market.

The remuneration percentage increase is in line with the increase in PAT

| Financial Year | No. of Employees | Growth in median remuneration | Growth in profits |

|---|---|---|---|

| FY22 | 270 | 10.01% | 25% |

| FY23 | 295 | 8.99% | 20% |

Strengths:

- Premium Quality Standard: They are an ISO: 9001-2008 Company

- Robust distribution network: Their offices are spread over all the major cities in India with a vast network of Distributors and Retailers for the domestic market and they are exporting their products to over 25 countries across the globe

- Vast Variety: They have various ranges of PVC products with different properties, patterns, designs & colours which fulfil the exclusive requirement

- Modern Calendaring Lines: The Factory houses modern Calendaring lines along with matching printing, lamination and tile-cutting facilities, all imported from the U.S.A

- Significant reduction in competition: The below-highlighted competitors (mentioned by CRISIL Credit rating in Nov 2018) are either not able to perform or are delisted.

- Consistency: Since 2001 they have won consecutive awards for exporting quality products to over 25 countries across the globe.

Weakness:

- Margins fluctuation may happen: PVC resin, the basic raw material, is a crude oil derivate. Hence, its price remains vulnerable to fluctuation in crude oil prices.

Financial Analysis

Consistently sales, OPM, Operating Profit and PAT are increasing

Good CAGR growth for sales and profit

Consistent ROEs for a very long period

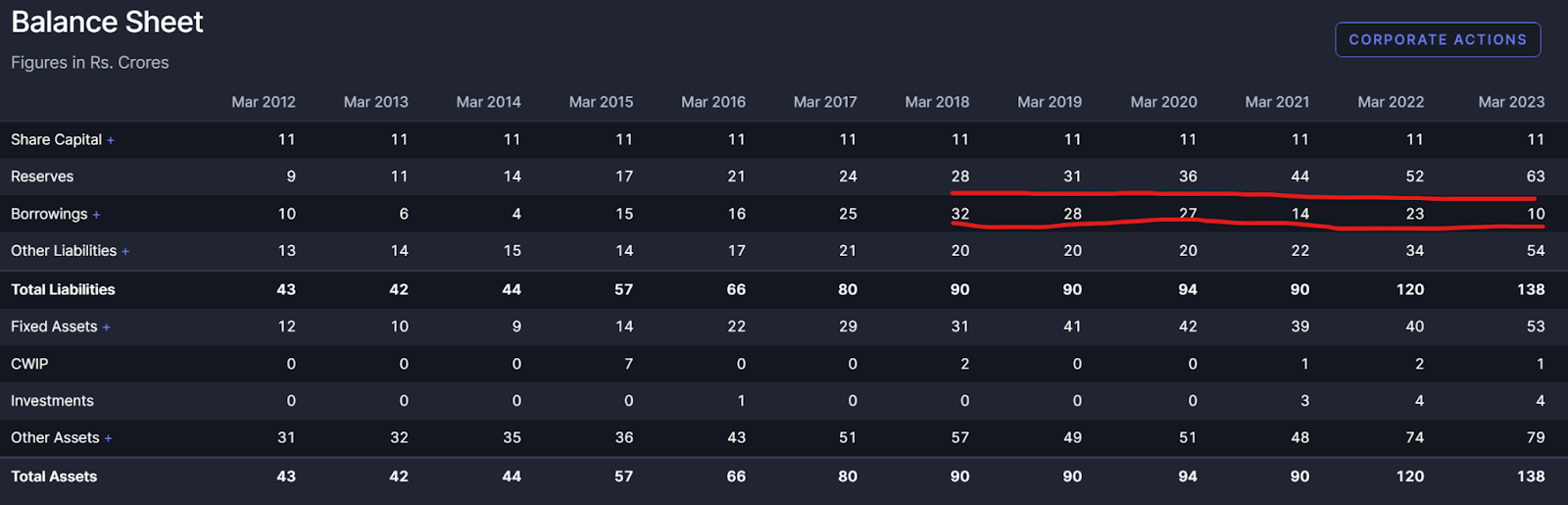

No equity dilution, consistently decreasing borrowings and increasing company reserves

Cash and Cash equivalents – 4.78 Cr

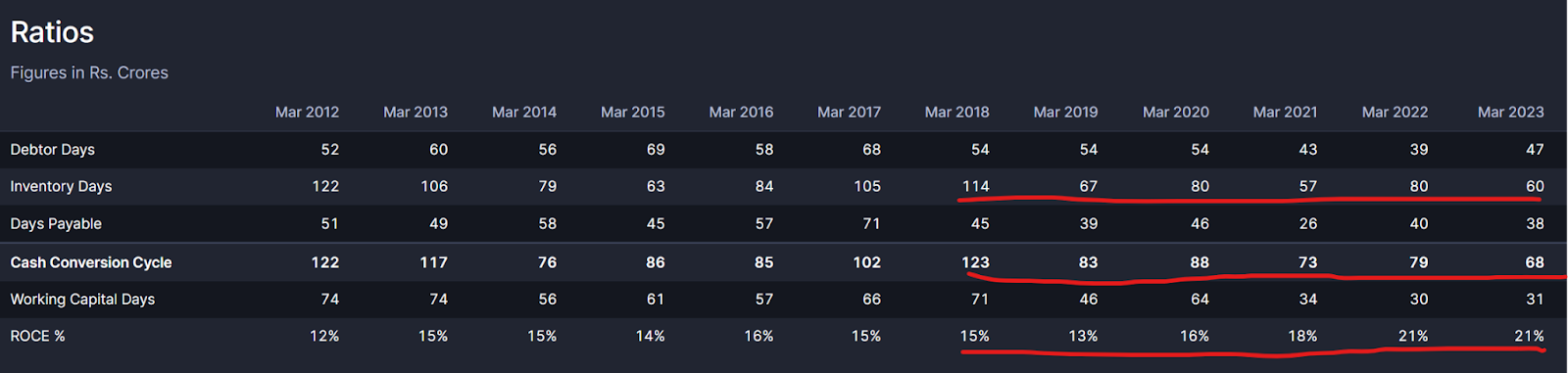

Significant reduction in Inventory Days and Cash Conversion Cycle resulting in better cash flows and ROCE

Why PrudentParrot finds this company interesting?

- Chance of Margin Expansion:

The primary raw material is Polyvinyl. The chart shows the price fluctuations of the same. The prices have stabilised at the lowest levels in the last 10 years.

The effect of this will be in the Margins of the company if they are able to take advantage of this.

Undervaluation: There is a good Margin of Safety

Bull Case:

Assuming that the sales grow by 20% in FY24 i.e. – 305Cr

If the company is able to expand its margin by 1% or 2%. The Operating Profit becomes – 36.5 Cr which is a 58% increase from FY23.

PEG becomes – 15/58 = 0.25 | Current PEG = 0.76. This means around 3x returns from here

Bear Case:

Assuming that the sales grow by 15% in FY24 i.e. – 292Cr

And there is no increase in margins. The Operating Profit becomes – 29.21 Cr which is a 27% increase from FY23.

PEG becomes – 15/27 = 0.55 | Current PEG = 0.76. This means around 1.5x returns from here

- Higher Capacity Utilisation: Presently, the company’s production capacity of its plant is ~16200 MT per year. But the company produced ~23,414 M.T. of PVC flooring, Sheetings, Films etc. because the company achieved higher capacity utilization with the installation and utilization of new Plant and machinery

- Improving Return Ratios: Improving working capital cycle resulting in good ROEs and ROCEs

- High Promoter holding: Strong Promoter holding around 67.5% showing their skin in the game.

- Paying dividends since 2016: Demonstrating its commitment to providing returns to shareholders and enhancing shareholder value.

FY23 Annual Report Analysis

- The management claims that the market for vinyl flooring, and sheeting is growing at 10-12% annually.

- The company has set up a new 4500 MT plant in UP.

- Future Plan – The company has stayed updated with the latest technologies to build up capabilities. Their plan is to explore ways to lower operating costs by modernisation of equipment and adding new products.

- The company has taken a term loan of Rs. 5 cr for the purpose of expansion. They claim that their current lines of credit are sufficient to meet their short to medium-term expansion plans.

- Risk and Concerns – The management says that dumping of finished goods in the market at cheaper rates by foreign companies may affect the profitability of the company.

- The management has also shown concern about the rising demand for PVC resin in India, which is the most important raw material for Premier Polyfilms. However, the supply is still not adequate to meet the growing demand.

- Moreover, for certain grades of resins used by the company, only a handful number of manufacturers are present in the country. Any disruption in its supply chain may affect the operations of the company adversely.

See you next time.

Until then… Stay Prudent!

Disclaimer: This article is provided for informational purposes only and should not be considered investment advice.